October 02, 2024

As the presidential election closes in, investors may be wondering how the outcome will affect their portfolios. History demonstrates that the market can gain under any kind of presidency and Congress, but individual sectors and industries may be impacted — for better or worse. This guide explores what those sector effects may look like through the lens of four topics addressed in our companion article, Election 2024: Themes to Watch. In our view, the policies that will most determine how specific sectors may respond to either a Vice President Harris or former President Trump administration are: 1) trade and tariffs, 2) taxes, 3) immigration as it relates to the labor market and 4) Federal Trade Commission (FTC) changes due to their potential impact on mergers and acquisitions (M&A).

Keeping these themes in mind, we analyze the sectors that we believe will be most affected.

Technology

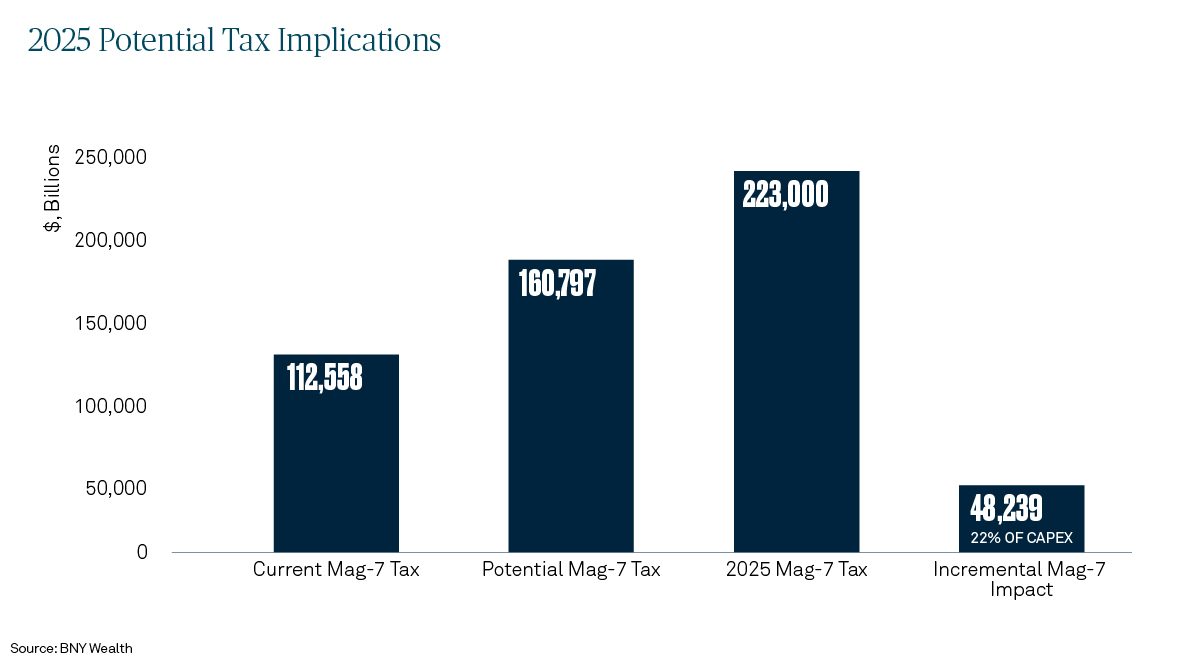

On a relative basis, the technology industry has a very attractive tax profile due to companies’ ownership of intellectual property in multiple jurisdictions and the more geographically diversified revenue profile many players possess. In a Harris-led scenario of higher tax rates, we estimate the Magnificent Seven would pay a tax rate of approximately 24% if rates moved to 28%, causing a $48 billion increase in tax liabilities. While seemingly trivial given the Magnificent Seven will generate approximately $2.3 trillion in revenue in 2025, it would equate to 22% of expected capital expenditures as the chart illustrates. In this context, greater tax liabilities could be detrimental, particularly when considering how important capital expenditures are for the future growth of this cohort.

Additionally, changes to the FTC and Department of Justice (DOJ) will be meaningful. The FTC and DOJ have taken a more active approach in the Technology industry, particularly when it involves M&A, consumer data and monopolistic behavior. The industry has seen a change in M&A activity such that transaction value declined by 60% in 2023. The FTC and DOJ are also suggesting more disruptive remedies among technology companies.

Healthcare

Within Healthcare, the four election-related factors we expect to have the greatest impact on equities are: 1) corporate tax rates, 2) potential changes in the managed care space, 3) drug price regulations and 4) potential changes at the FTC.

We see managed care, hospitals and drug distributors as most exposed to corporate taxes given that nearly 100% of industry profits are generated in the U.S. If Harris were to raise corporate taxes, large cap multinational drug and medical device companies would likely be able to use outside U.S. tax shelters to mitigate the impact, thereby leaving cash flows mostly intact. However, in this scenario, multinationals would likely see cash become trapped overseas, which would reduce funds available for U.S. investment and share buybacks.

The managed care industry would generally be better off under a Republican administration given its exposure to U.S. corporate tax rates as described above. Additionally, Republicans, including Trump, have historically supported more favorable Medicare Advantage rate updates, though they have also favored more restrictive Medicaid requirements and scaling back the Affordable Care Act exchanges. Harris has talked about cracking down on the practices of pharmacy benefit managers that result in reduced pharmacy profitability and higher consumer costs, but she has not shared details on what a policy response might look like.

Both presidential candidates are also likely to attempt to implement some measure of drug price control though we believe new legislation is unlikely given the Congressional votes required. Trump could seek to repeal or minimize some elements of the Inflation Reduction Act (IRA) drug price cuts, which would be positive for the pharmaceutical industry, however, we think an IRA repeal is unlikely and furthermore would expect Trump to attempt to implement other types of drug price controls that would be negative for industry. Harris has talked about adding more drugs to the IRA-related drug price list and shortening the eligibility window; however, such changes would require legislation and thus we view them as improbable.

Lastly, a more lenient FTC under Trump could facilitate a more active healthcare dealmaking environment.

Consumer Discretionary

Lower corporate tax rates under Trump would benefit the entire group but names in the Restaurants, Lodging, Regional Gaming and Hardlines/Broadlines/Grocery spaces with heavy U.S. profit exposure would benefit the most.

Higher taxes on high-income households under Harris could dampen luxury goods spending but expansion of the child tax credit, food stamps, Medicaid and student loan forgiveness could benefit the retail space.

Under Trump, higher tariffs could have a negative effect on companies that import goods for domestic consumption. Risk of higher freight rates and tariff escalation will mainly impact Discretionary/General Merchandise imports (much of Retail), with some of the most exposed categories being 1) Toys/Games/Sporting Goods, 2) Consumer Electronics, 3) Footwear, 4) Home Furnishings, 5) Household Appliances and 6) Apparel. The risk of higher freight rates and tariff escalation is lower in Restaurants, but companies with China operations could be affected.

Tighter immigration rules could limit the labor pool, thereby increasing labor costs. Within Consumer Discretionary, sectors with the highest reliance on U.S. labor include Hardlines, Broadlines and Restaurants. We’d expect a potentially higher minimum wage under Harris to have a similar impact as tighter immigration standards.

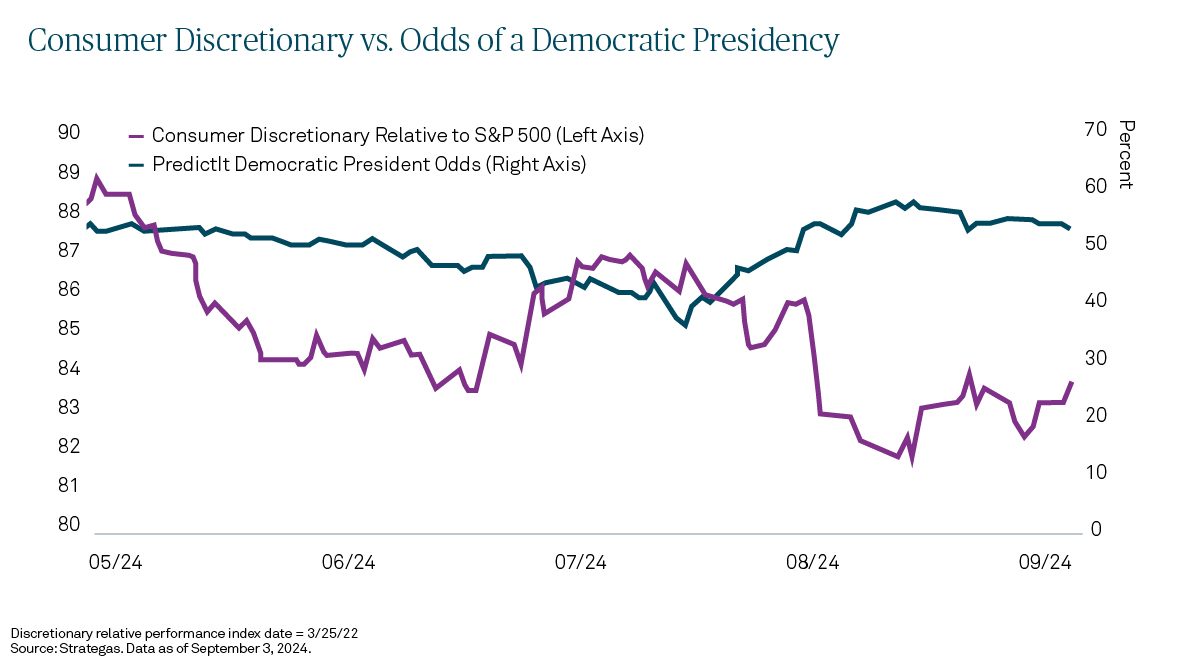

The chart below shows that Consumer Discretionary stocks have underperformed the S&P 500 modestly since Harris’ presidential candidacy was announced, perhaps reflecting concerns that a Democratic President could result in higher corporate taxes and employee wages.

Consumer Staples

Lower taxes would benefit the entire group, but Staples, Food and Retail names would have more exposure than Beverages to potentially higher taxes under Harris given a higher percentage of domestic sales. Household & Personal Care names tend to have more multinational exposure than Food & Beverage, and as a result are less exposed to U.S. corporate tax rates.

Expansion of the child tax credit, food stamps, Medicaid and student loan forgiveness could drive higher Staples spending.

Beverage names could have more tariff exposure than Food due to higher aluminum exposure. Retailers that rely heavily on overseas suppliers could also have higher tariff exposure under Trump.

Tighter immigration rules could limit the labor pool, thereby increasing labor costs. Within Staples subsectors, Food and Retail names have the highest reliance on U.S. labor. Household & Personal Care and Beverages are less exposed than food but would still be impacted. We’d expect a potentially higher minimum wage under Harris to have a similar impact as tighter immigration standards.

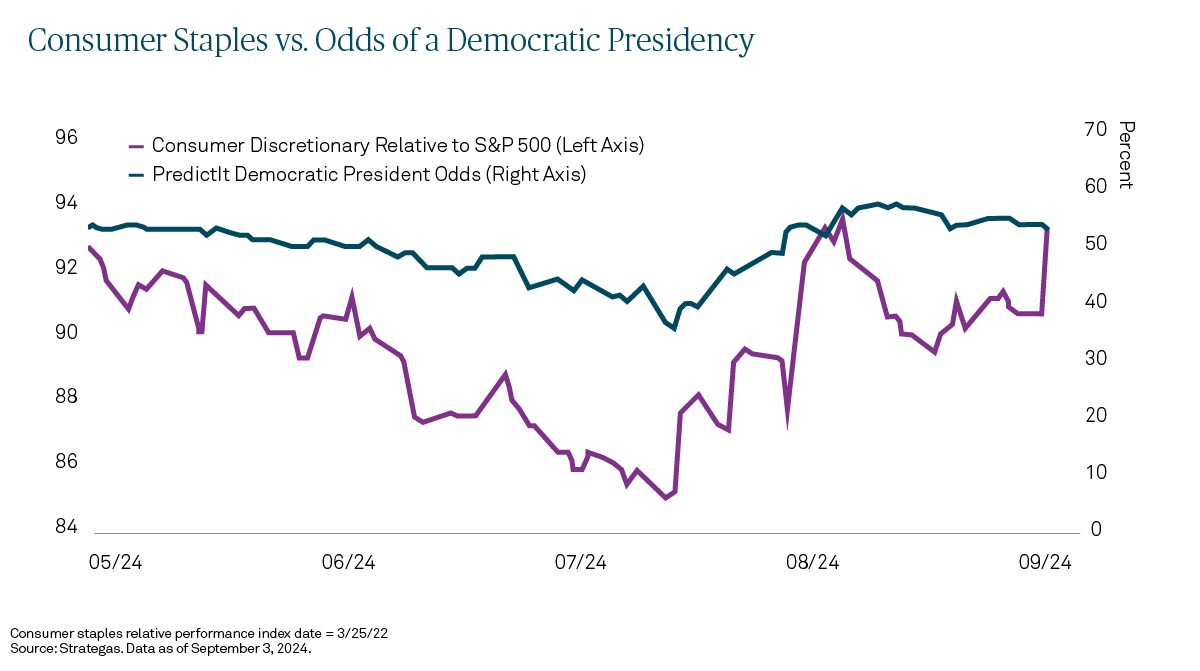

Consumer Staples stocks have outperformed the S&P 500 since July, coinciding with Harris being named the Democratic presidential candidate. This may reflect a view that tariff and immigration risk are likely to be lower under Harris than Trump, though we note that other defensive sectors (Utilities and Healthcare) have also significantly outperformed the benchmark over this time as funds rotated out of the Magnificent Seven.

Financial Services

The Financial Services sector generates most of its earnings domestically, so the sector would be one of the most exposed to a higher federal income tax rate.

A Harris administration would likely continue to increase capital requirements for and apply more stringent rules to smaller banks. The Consumer Financial Protection Bureau under Harris would likely continue its focus against a variety of fees that banks and finance companies charge. A Trump administration would appoint more industry-friendly regulators who would propose far fewer new rules.

Energy

The factors we are focusing on within the Energy sector are commodity prices and the IRA.

While Trump’s pro-drilling stance is supportive of industry activity, it tends to lead to oversupply and lower oil and natural gas prices, which reduce profits. Trump is likely to push OPEC to bring back some oil production that has been held offline since Covid, similar to what he did in late 2019. This could push oil prices lower. However, Trump is also likely to accelerate approvals for U.S. liquefied natural gas exports, which would provide a sustainable demand outlet for U.S. natural gas producers and help bring U.S. prices toward international prices.

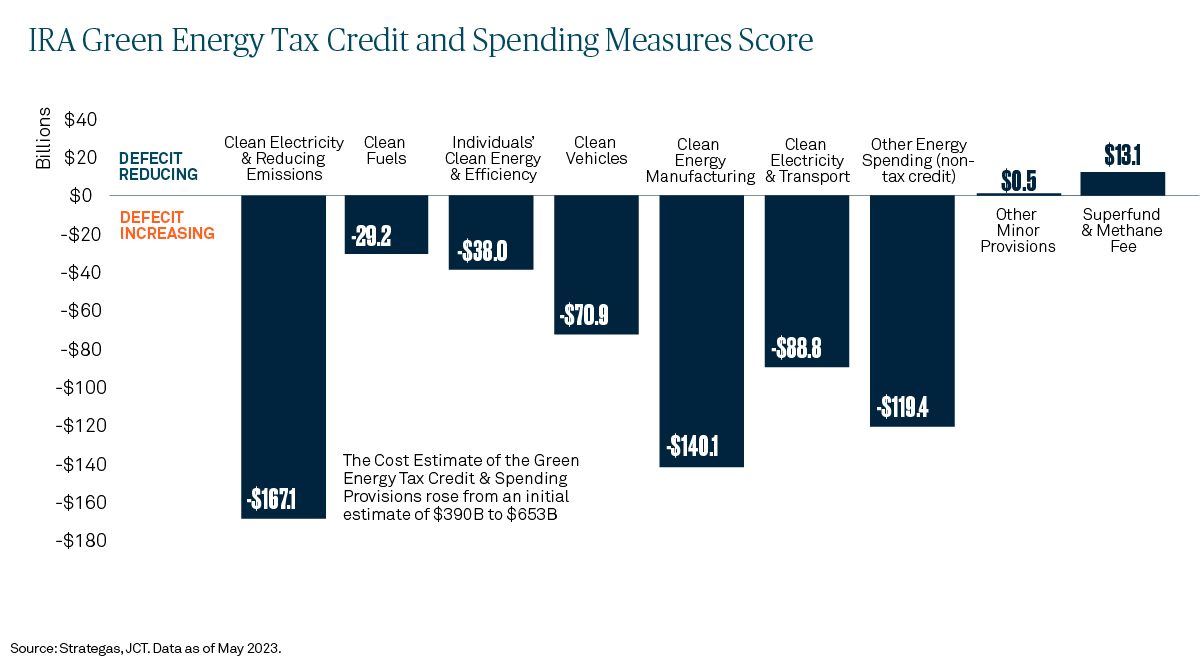

The IRA was passed in August 2022 under the Biden/Harris administration and provides billions of dollars of tax credits to support renewable energy development. The chart below depicts the effects of the IRA on the nation’s deficit as of May 2023, when the Congressional Budget Office updated the cost of these provisions from $390 billion in 2022 to $653 billion. The increase reflects the higher-than-expected number of projects announced because of these generous incentives. Harris is likely to preserve these credits to support green energy projects. However, if Trump needs to identify spending offsets to maintain his TCJA tax cuts, he may seek to reduce the $7,500 electric vehicle credit and the production tax credits allocated to the wind industry.

Industrials

Tariff policy is the biggest factor here. We believe Trump could disrupt global trade with his aggressive stance on China. While tariffs would benefit domestic manufacturers of imported goods, they may also lead to a slowdown in global growth. We would also expect friction across global supply chains, which ends up delaying projects and increasing the need for higher working capital to ensure inventory reliability. On the other hand, these policies should support domestic manufacturing, rails and trucking.

The IRA plays an important role for this sector as well. Electrical equipment and HVAC companies have enjoyed substantial revenue and backlog growth due to the IRA’s subsidies for clean energy. Stripping these benefits away under Trump would be a huge blow to these industries.

On Defense, Trump is less likely to involve the U.S. in international conflicts and has been critical of the amount of U.S. support there is for NATO, according to Dan Caldwell, a vice president at the Trumpist Center for Renewing America, in POLITICO¹.

Materials

Tariffs and the IRA play key roles in this sector. If Trump reduces subsidies from the IRA, we would expect lower demand for copper, aluminum and lithium as the electrification trend slows down. But he would likely soften many of the emission rules from Biden’s term, which would support coal. Further, Trump’s tariffs would support steel prices and his intent to exploit U.S. resources could help the nascent rare earth industry. Harris is likely to increase emission rules on this high-polluting sector and an increase in corporate taxes would further impact what is already a low-return space.

Utilities

Electric utilities are benefiting from rising demand for power as the U.S. economy electrifies, supply chains deglobalize and data center growth accelerates to support artificial intelligence. Trump is more likely than Harris to accelerate the reshoring trend but is less supportive of electrifying the economy, which is a major driver of future earnings growth. Trump would also soften emission rules on the sector, which could help increase power generation capacity and keep a lid on electricity prices, which benefit regulated utilities.

Trump’s China tariffs would likely increase solar panel prices, which could slow clean energy development and earnings growth for the sector.

The Bottom Line

As we approach election day, we may see a pickup in market volatility, especially at the sector level. This may create opportunities for our equity managers as they continue to assess the potential impact to sectors and industries and seek to uncover bottom-up opportunities based on the expected winners and losers of each candidate’s policy platform. Ultimately, the makeup of Congress will have a significant impact on the ability of the next president to adopt the policies laid out in their platform.

1https://www.politico.com/news/magazine/2024/07/02/nato-second-trump-term-00164517

This material is provided for illustrative/educational purposes only. This material is not intended to constitute legal, tax, investment or financial advice. Effort has been made to ensure that the material presented herein is accurate at the time of publication. However, this material is not intended to be a full and exhaustive explanation of the law in any area or of all of the tax, investment or financial options available. The information discussed herein may not be applicable to or appropriate for every investor and should be used only after consultation with professionals who have reviewed your specific situation.

The Bank of New York Mellon, DIFC Branch (the “Authorized Firm”) is communicating these materials on behalf of The Bank of New York Mellon. The Bank of New York Mellon is a wholly owned subsidiary of The Bank of New York Mellon Corporation. This material is intended for Professional Clients only and no other person should act upon it. The Authorized Firm is regulated by the Dubai Financial Services Authority and is located at Dubai International Financial Centre, The Exchange Building 5 North, Level 6, Room 601, P.O. Box 506723, Dubai, UAE.

The Bank of New York Mellon is supervised and regulated by the New York State Department of Financial Services and the Federal Reserve and authorized by the Prudential Regulation Authority. The Bank of New York Mellon London Branch is subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority. Details about the extent of our regulation by the Prudential Regulation Authority are available from us on request. The Bank of New York Mellon is incorporated with limited liability in the State of New York, USA. Head Office: 240 Greenwich Street, New York, NY, 10286, USA.

In the U.K. a number of the services associated with BNY Wealth’s Family Office Services– International are provided through The Bank of New York Mellon, London Branch, One Canada Square, London, E14 5AL. The London Branch is registered in England and Wales with FC No. 005522 and BR000818.

Investment management services are offered through BNY Mellon Investment Management EMEA Limited, BNY Mellon Centre, One Canada Square, London E14 5AL, which is registered in England No. 1118580 and is authorized and regulated by the Financial Conduct Authority. Offshore trust and administration services are through BNY Trust Company (Cayman) Ltd.

This document is issued in the U.K. by The Bank of New York Mellon. In the United States the information provided within this document is for use by professional investors.

This material is a financial promotion in the UK and EMEA. This material, and the statements contained herein, are not an offer or solicitation to buy or sell any products (including financial products) or services or to participate in any particular strategy mentioned and should not be construed as such.

BNY Mellon Fund Services (Ireland) Limited is regulated by the Central Bank of Ireland BNY Mellon Investment Servicing (International) Limited is regulated by the Central Bank of Ireland.

Trademarks and logos belong to their respective owners.

BNY Wealth conducts business through various operating subsidiaries of The Bank of New York Mellon Corporation. BNY and Bank of New York Mellon are corporate names of The Bank of New York Mellon Corporation and may be used to reference the corporation as a whole and/or its various subsidiaries generally.

©2024 The Bank of New York Mellon. All rights reserved. WI-611000-2024-09-24