October 02, 2024

Election season is heating up, creating uncertainty in the markets as many investors consider which candidate will help — or hinder — equities more. However, history tells us that economic fundamentals drive market performance much more than who sits in the White House. In contrast, individual sectors and industries may be affected by a candidate’s proposed policies. Party differences around four main themes will likely have the greatest impact at a sector level. The themes we note are trade and tariffs, taxes, immigration as it relates to the labor market and Federal Trade Commission (FTC) changes due to their potential effect on mergers and acquisitions (M&A).

Because the race is currently so close, we expect to see volatility in equities leading up to the election as investors express their views on who will win. Once the new president and the composition of Congress are confirmed, we anticipate the market may price in some of the insights of this article, which analyzes how the four key themes may affect S&P sectors.

The themes:

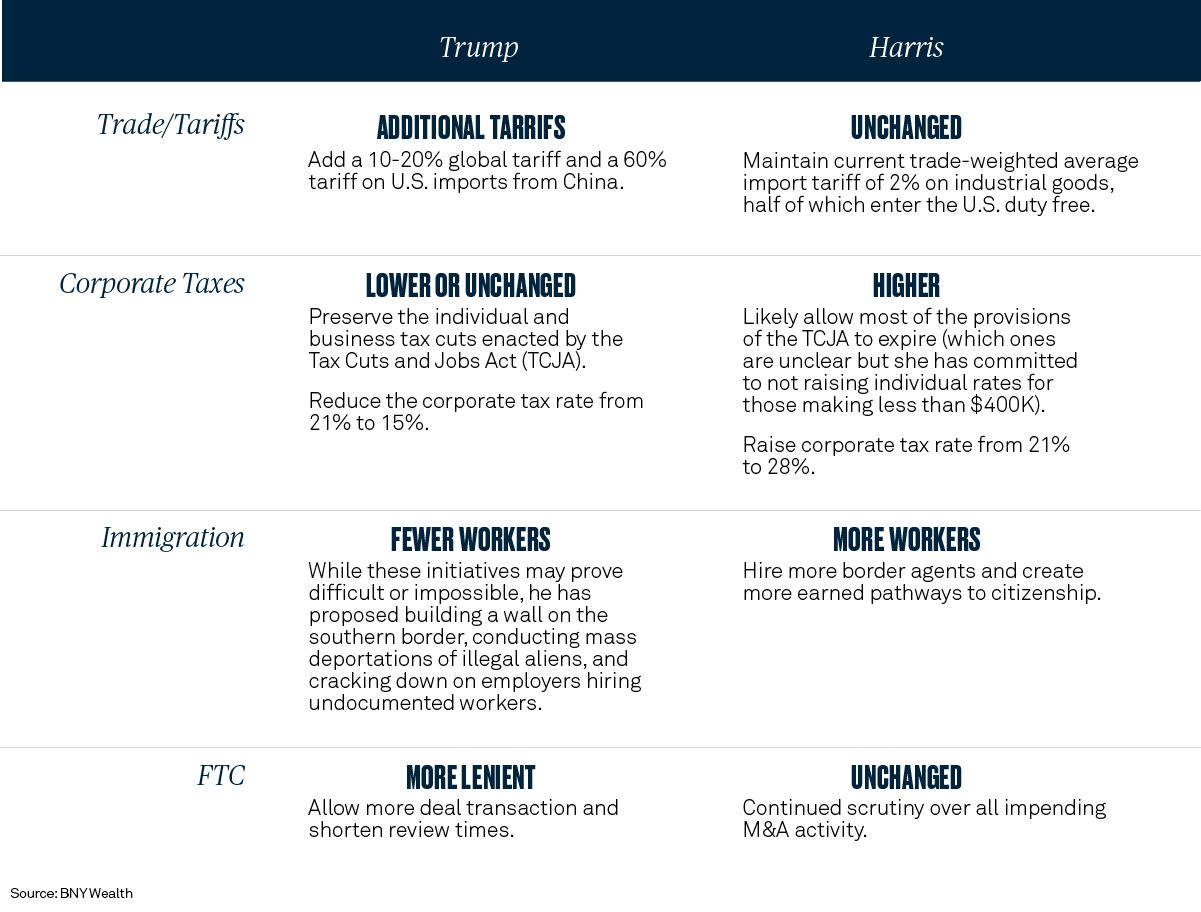

1. Trade/Tariffs

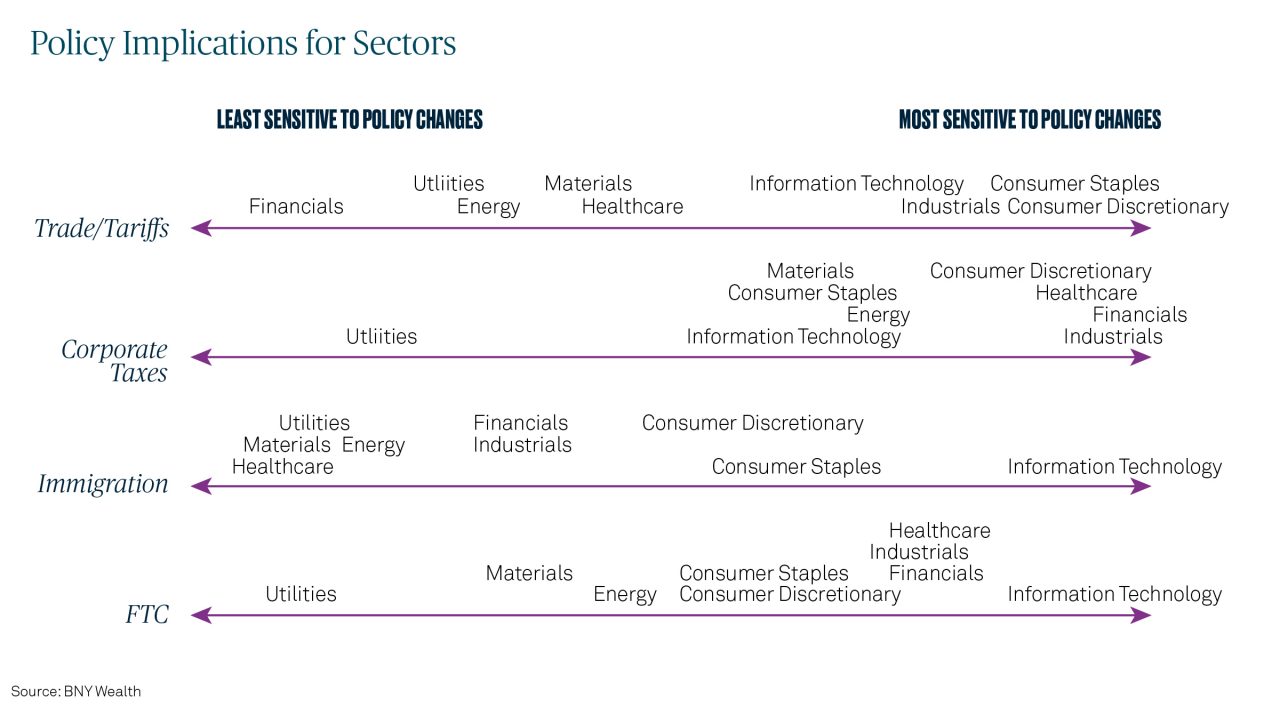

Many expect that Vice President Harris would maintain the status quo, which already includes tariffs on solar panels, steel, aluminum and goods from China, whereas former President Trump is likely to be aggressive. In the presidential debate, he indicated he might implement a 10-20% global tariff as well as a 60% tariff on U.S. imports from China. A president does have the authority to impose tariffs on his or her own, so it will be important to consider the potential impact they may have on inflation and global growth. The Consumer Discretionary and Consumer Staples sectors will likely be most affected by changes in trade policies.

2. Corporate Taxes

The candidates are truly divergent on this issue. Trump will focus on maintaining or lowering corporate and personal taxes, whereas Harris has a more progressive approach to tax structure. During his term, Trump lowered corporate taxes from 35% to 21% and has mentioned lowering them again to 15%. Harris, on the other hand, previously indicated she would raise corporate taxes to 28%, according to CNBC and other news sources, although it is possible she encounters opposition in Congress. A higher corporate tax rate may adversely affect businesses across sectors.

3. Immigration

Trump will likely institute stricter immigration policies and while many expect Harris not to deviate from the status quo, she has toughened her stance while campaigning. Limits on immigration could drive inflation upward through higher wages, and immigration policy will have an acute effect on sectors such as Consumer Staples and Information Technology.

4. The FTC and M&A

The president appoints the FTC Chair and in its current form, the FTC has had a restrictive bent, making it difficult for companies to make meaningful acquisitions. M&A activity can help companies improve their competitiveness in several ways, such as allowing them to achieve economies of scale, diversify their businesses, and enter new markets. We would expect a more lenient FTC under Trump than under Harris, which would benefit sectors that rely on M&A like Information Technology, Financials and Healthcare.

In summary, we expect the following:

See the chart below for a more comprehensive look at how different sectors may be exposed to potential policy change. Still, the impact on sectors will depend considerably on the composition of Congress and what becomes law, as it is often very different than what is proposed on the campaign trail.

The Bottom Line

It is important to remember that historically the outcome of a presidential election hasn’t affected the aggregate market significantly as stocks can and have moved higher under all types of administrations. Don’t let campaign proposals influence your investment decisions because those policies often look different once a candidate takes office, frequently due to the checks and balances of Congress. Stick with your long-term investment plan aligned to your wealth goals; we believe it’s the best approach for navigating any near-term volatility that materializes as election day draws closer.

This material is provided for illustrative/educational purposes only. This material is not intended to constitute legal, tax, investment or financial advice. Effort has been made to ensure that the material presented herein is accurate at the time of publication. However, this material is not intended to be a full and exhaustive explanation of the law in any area or of all of the tax, investment or financial options available. The information discussed herein may not be applicable to or appropriate for every investor and should be used only after consultation with professionals who have reviewed your specific situation.

The Bank of New York Mellon, DIFC Branch (the “Authorized Firm”) is communicating these materials on behalf of The Bank of New York Mellon. The Bank of New York Mellon is a wholly owned subsidiary of The Bank of New York Mellon Corporation. This material is intended for Professional Clients only and no other person should act upon it. The Authorized Firm is regulated by the Dubai Financial Services Authority and is located at Dubai International Financial Centre, The Exchange Building 5 North, Level 6, Room 601, P.O. Box 506723, Dubai, UAE.

The Bank of New York Mellon is supervised and regulated by the New York State Department of Financial Services and the Federal Reserve and authorized by the Prudential Regulation Authority. The Bank of New York Mellon London Branch is subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority. Details about the extent of our regulation by the Prudential Regulation Authority are available from us on request. The Bank of New York Mellon is incorporated with limited liability in the State of New York, USA. Head Office: 240 Greenwich Street, New York, NY, 10286, USA.

In the U.K. a number of the services associated with BNY Wealth’s Family Office Services– International are provided through The Bank of New York Mellon, London Branch, One Canada Square, London, E14 5AL. The London Branch is registered in England and Wales with FC No. 005522 and BR000818.

Investment management services are offered through BNY Mellon Investment Management EMEA Limited, BNY Mellon Centre, One Canada Square, London E14 5AL, which is registered in England No. 1118580 and is authorized and regulated by the Financial Conduct Authority. Offshore trust and administration services are through BNY Trust Company (Cayman) Ltd.

This document is issued in the U.K. by The Bank of New York Mellon. In the United States the information provided within this document is for use by professional investors.

This material is a financial promotion in the UK and EMEA. This material, and the statements contained herein, are not an offer or solicitation to buy or sell any products (including financial products) or services or to participate in any particular strategy mentioned and should not be construed as such.

BNY Mellon Fund Services (Ireland) Limited is regulated by the Central Bank of Ireland BNY Mellon Investment Servicing (International) Limited is regulated by the Central Bank of Ireland.

Trademarks and logos belong to their respective owners.

BNY Wealth conducts business through various operating subsidiaries of The Bank of New York Mellon Corporation. BNY and Bank of New York Mellon are corporate names of The Bank of New York Mellon Corporation and may be used to reference the corporation as a whole and/or its various subsidiaries generally.

©2024 The Bank of New York Mellon. All rights reserved. WI-612088-2024-09-26